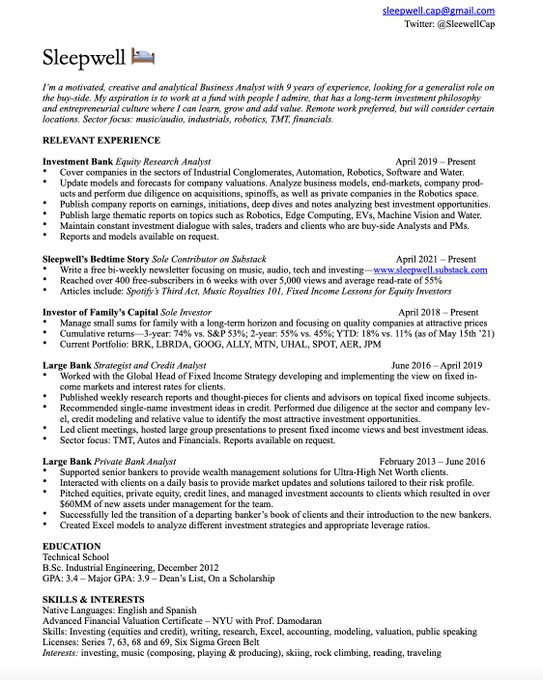

Sleepwell🛌

@SleepwellCap

21,831

Followers

615

Following

1,407

Media

13,078

Statuses

Looking for investments to sleep well. Mostly Music, Tech, Financials & Luxury. Musician and engineer. Opinions my own, please see disclaimers on Substack.

Don't wanna be here?

Send us removal request.