Hilary Allen

@ProfHilaryAllen

3,499

Followers

262

Following

10

Media

860

Statuses

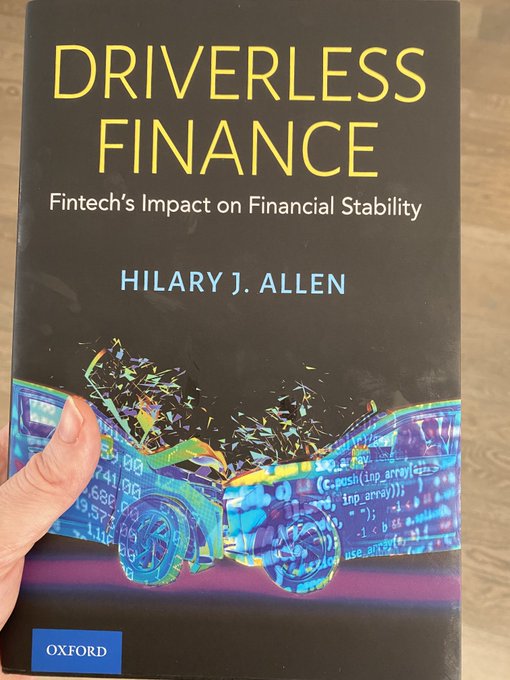

Professor of financial regulation, American University pessimistic financial futurist #driverlessfinance

Joined July 2021

Don't wanna be here?

Send us removal request.